|

|

Mid Career

- Mid-Career Retirement Planning

At this point in your career you should be actively making decisions to ensure retirement well-being. It is important to know what steps you should be taking now and how some benefits transition into retirement so you can set yourself up for a comfortable life after you leave the workforce.

Steps you should be taking now:

- Educate yourself on retirement, motivate yourself to save. “The Ultimate Retirement Planning Guide”

- Use the EBIS Quick Retirement Calculator to start doing estimates on FERS Pension payments at various ages and length of service.

- Collect your official Social Security Benefits estimates.

- Consider Roth vs Traditional IRAs and 401Ks.

- Consider outside investments. Start trying to pay off your home mortgage.

- Start getting official Retirement Estimates from ABC 10 years out to MRA.

Understanding how Federal Benefits effect you at retirement.

- Leave

Unused Sick Leave

All employees receive credit for the total number of unused sick leave hours accumulated until their day of retirement. Employees should be aware of three things with respect to the treatment of unused sick leave:

- Unused sick leave hours are added to their length of service;

- Unused sick leave credit is used only in the computation of a retiring employee's CSRS or FERS annuity. Employees who leave federal service and opt for a deferred retirement lose all of their unused sick leave at the time of their departure from federal service. Unused sick leave cannot be used to establish retirement eligibility or to calculate the high-three average salary.

- Unused sick leave is credited in 30 day increments towards your retirement.

- There is no limit on the amount of unused sick leave that can be credited.

Unused Annual Leave

In general, a retiring employee receives a lump sum payment for any unused annual leave when the employee retires from federal service, or if the employee leaves federal service to enter active military duty and elects to receive a lump sum payment. A lump sum payment will equal the pay the employee would have received had the employee remained employed until expiration of the period covered by the annual leave. An agency calculates a lump sum payment for a retiring employee by multiplying the number of hours of accumulated and accrued annual leave by the employee's applicable hourly rate of pay.

- FSA – Flexible Spending Accounts

- Health FSA - A Health Care FSA (HCFSA) is a pre-tax benefit account that's used to pay for eligible medical, dental, and vision care expenses that are not covered by your health care plan or elsewhere. With an HCFSA, you use pre-tax dollars to pay for qualified out-of-pocket health care expenses.

- Dependent Care FSA (DCFSA) - is a pre-tax benefit account used to pay for eligible dependent care services, such as preschool, summer day camp, before or after-school programs, and child or adult daycare. It's a smart and simple way to save money while taking care of your loved ones so that you can continue to work. With a DCFSA, you use pre-tax dollars to pay for qualified out-of-pocket dependent day care expenses. The money you contribute to a DCFSA is not subject to payroll taxes, so you end up paying less in taxes and taking home more of your paycheck.

- Limited Expense Health Care FSA (LEX HCFSA) - is a flexible spending account option if you are enrolled in a Federal Employees Health Benefits (FEHB) high-deductible health plan (HDHP) and have a Health Savings Account (HSA). This option is also available if your spouse is enrolled in a non-FEHB HDHP and has an HSA. IRS rules do not allow you to contribute to a Health Savings Account (HSA) if you are covered by any non-qualifying health plan, including a general-purpose Health Care FSA. By limiting FSA reimbursements to qualifying dental and vision care expenses, you and your spouse remain eligible to participate in both a LEX HCFSA and an HSA. Participating in both plans allows you to maximize your savings and tax benefits. The money you contribute to a LEX HCFSA is not subject to payroll taxes, so you pay less in taxes and take home more of your paycheck.

- FEHB - Federal Employees Health Benefits Program

You may continue your health insurance coverage only if you meet the following conditions:

- Your annuity must begin within 30 days or, if you are retiring under the Minimum Retirement Age (MRA) plus 10 provision of the Federal Employees Retirement System (FERS), health and life insurance coverages are suspended until your annuity begins, even if it is postponed.

- You must be covered for health insurance when you retire.

- You must have been continuously covered by the Federal Employees Health Benefits Program, TRICARE, or the Civilian Health and Medical Program for Uniformed Services (CHAMPUS):

- for five years immediately before retiring.

- during all of your federal employment since your first opportunity to enroll.

- continuously for full periods of service beginning with the enrollment that started before January 1, 1965, and ending with the date on which you become an annuitant, whichever is shortest.

- FLTCIP – Federal Long Term Care Insurance Program

The Federal Long Term Care Insurance Program (FLTCIP) provides long term care insurance to help pay for costs of care when enrollees need help with activities they perform every day, or you have a severe cognitive impairment, such as Alzheimer's disease.

Most Federal and U.S. Postal Service employees and annuitants, active and retired members of the uniformed services, and their qualified relatives are eligible to apply for insurance coverage under the FLTCIP.

Most employees must be eligible for the FEHB Program in order to apply for coverage under the FLTCIP. It does not matter if they are actually enrolled in FEHB - eligibility is the key. Annuitants do not have to be eligible or enrolled in the FEHB Program. Certain medical conditions, or combinations of conditions, will prevent some people from being approved for coverage. You must apply to find out if you are eligible to enroll.

For more information about the FLTCIP, please contact Long Term Care Partners at 1 800-582-3337, or visit the www.LTCfeds.com

- Medicare

Medicare has four parts: A, B, C, and D

- Today all federal employees will qualify for premium-free Part A when they turn 65. It helps pay for inpatient hospitalization and care at a skilled nursing facility following a hospital stay. Your FEHBP plan also covers hospitalization, skilled nursing care, home health care and hospice care. But having Medicare Part A can provide additional benefits that your FEHBP plan may not cover and your FEHBP plan may waive some or all of your out-of-pocket inpatient expenses when Medicare Part A becomes the primary payer.

- Part B is where the decision-making process can get tricky. It covers outpatient services, such as treatment at a doctor's office. If your FEHBP plan will continue to cover you when you are 65 and older, why do you need to pay an additional health insurance premium for Medicare Part B? Part B is expensive. Its cost is not covered by payroll taxes, but instead paid for through premiums shared by the enrollee and the federal government. For most beneficiaries, the government pays about 75 percent of the Part B premium, and the beneficiary pays the remaining 25 percent. {The standard Part B premium amount in 2019 is $135.50.}

- Most federal employees and retirees who are covered under FEHBP do not need to enroll in Part C (Medicare Advantage) and Part D (which covers prescription drugs).

- Social Security

Social Security benefits are based on earnings averaged over most of a worker's lifetime. Your actual earnings are first adjusted or "indexed" to account for changes in average wages since the year the earnings were received. Then the Social Security Administration calculates your average monthly indexed earnings during the 35 years in which you earned the most. The Social Security Administration applies a formula to these earnings and arrives at your basic benefit, or "primary insurance amount" (PIA). This is the amount you would receive at your full retirement age.

You can calculate your estimated earnings at: https://www.ssa.gov/planners/calculators/

- Federal Annuity

FERS Basic Annunity is computed based on your length of service and “high-3” average salary. Your basic pay is the salary you earn for your position. It does not include payments for overtime, bonuses, etc.

FERS Basic Annuity Formula

| AGE | FORMULA |

| If age 62 or older at retirement with less than 20 years of service, OR under the age of 62 and qualified for an immediate voluntary retirement

|

1 percent of your high-3 average salary for each year of service |

| If age 62 or older with 20 or more years of service

|

1.1 percent of your high-3 average for each year of service. |

- Thrift Savings Plan (TSP)

The Thrift Savings Plan (TSP) is a retirement savings and investment plan for Federal employees and members of the uniformed services, including the Ready Reserve. It was established by Congress in the Federal Employees' Retirement System Act of 1986 and offers the same types of savings and tax benefits that many private corporations offer their employees under 401(k) plans.

You may not have been paying much attention to your TSP account since you came on board. But early to mid career is a great time to make sure your money is working for you. Research the different funds and decide which one is right for you.

Investment Funds:

- G Fund: Govt Securities – average of 4+ years to maturity

- F Fund: Fixed Income Bonds (Barcleys Capital US Aggregate Bond Index)

- C Fund: Common Stock (S&P 500 Stock Index)

- S Fund: Small Cap Stock (Dow Jones US Completion Stock Index, No S&P 500)

- I Fund: International Stock (MSCI EAFE Index (Europe, Australasia, Far East))

Life Cycle Funds:

These funds use professionally determined investment mixes that are tailored to meet investment objectives based on various time horizons. The objective is to strike an optimal balance between the expected risk and return associated with each fund.

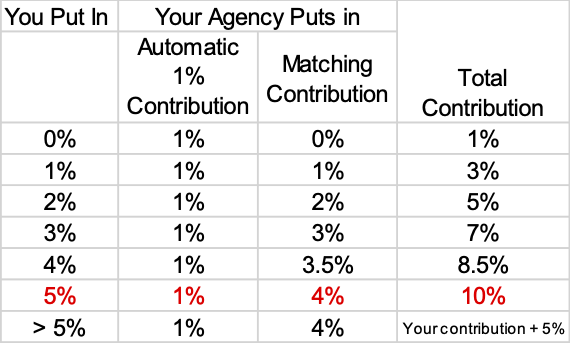

The government matches your contributions up to 5%. You should be at the very least investing 5% to get your matching contributions. It is wise with each promotion you get to increase your contributions.

For more information please visit www.tsp.gov

Helpful Links

|

|

Home

At a Glance

News / Current Issues

Policy & Procedures

Program Summary

FAQs

Good Enough to Share

Lessons Learned

Archives

Related Sites

Training

References

Division & District POCs

Find a Job

Mid-Career

On-Boarding

Becoming a Supervisor

Learn Your Job

Retirement

Master Your Job

Mid Career

Trainings

LDP

PDT and CoP

Updating your Resume

Dealing with Burn Out

Balancing Work and Family

Mid Career Retirement Planning

|